Managing Concentrated Stock: What Anthropic, SpaceX, and OpenAI Employees Should Know

Working with employees at companies like Anthropic, SpaceX, and OpenAI, we've had some version of the same conversation many times. An IPO is announced or approaching, the equity that's been accumulating for years starts to feel real, and the first question is usually some version of: what do I actually do with this now?

The theory isn't the hard part. Most people in this situation already understand that holding the majority of their net worth in one stock carries meaningful risk. The harder part is the execution: figuring out how much to sell, when, at what tax cost, and what options exist for someone who's in a lock-up period, or who has the ability to sell but isn't ready to yet.

There's a saying that comes up often in financial planning: concentration makes you rich, but diversification keeps you rich. This post is an attempt to make that tension practical. We'll walk through the main approaches — selling outright, direct indexing, options strategies, and securities-backed lending — what each one actually involves, and what the trade-offs are. The right answer depends on things specific to your situation, but knowing what's available is a reasonable place to start.

Why Concentration Risk Is Worth Taking Seriously

Owning a large position in a single company doesn't feel like a problem when the company is doing well. It tends to start feeling like one when something changes.

Amazon employees who held concentrated positions in 2000 watched the stock fall from roughly $118 to around $6 per share over the following two years. The company survived and went on to be worth far more. The people who held through that decline were living with serious paper losses for years, and some had to sell at the wrong time to meet other needs, making the losses permanent.

Anthropic, SpaceX, and OpenAI may be exceptional companies. That doesn't insulate a concentrated equity position from the basic dynamics of single-stock risk. If one position represents 60%, 70%, or 90% of your net worth, your financial picture isn't really a portfolio… It's a bet. Your bet may well pay off, but if it doesn’t, it comes at a big cost.

So what do you do with it?

The Traditional Approaches

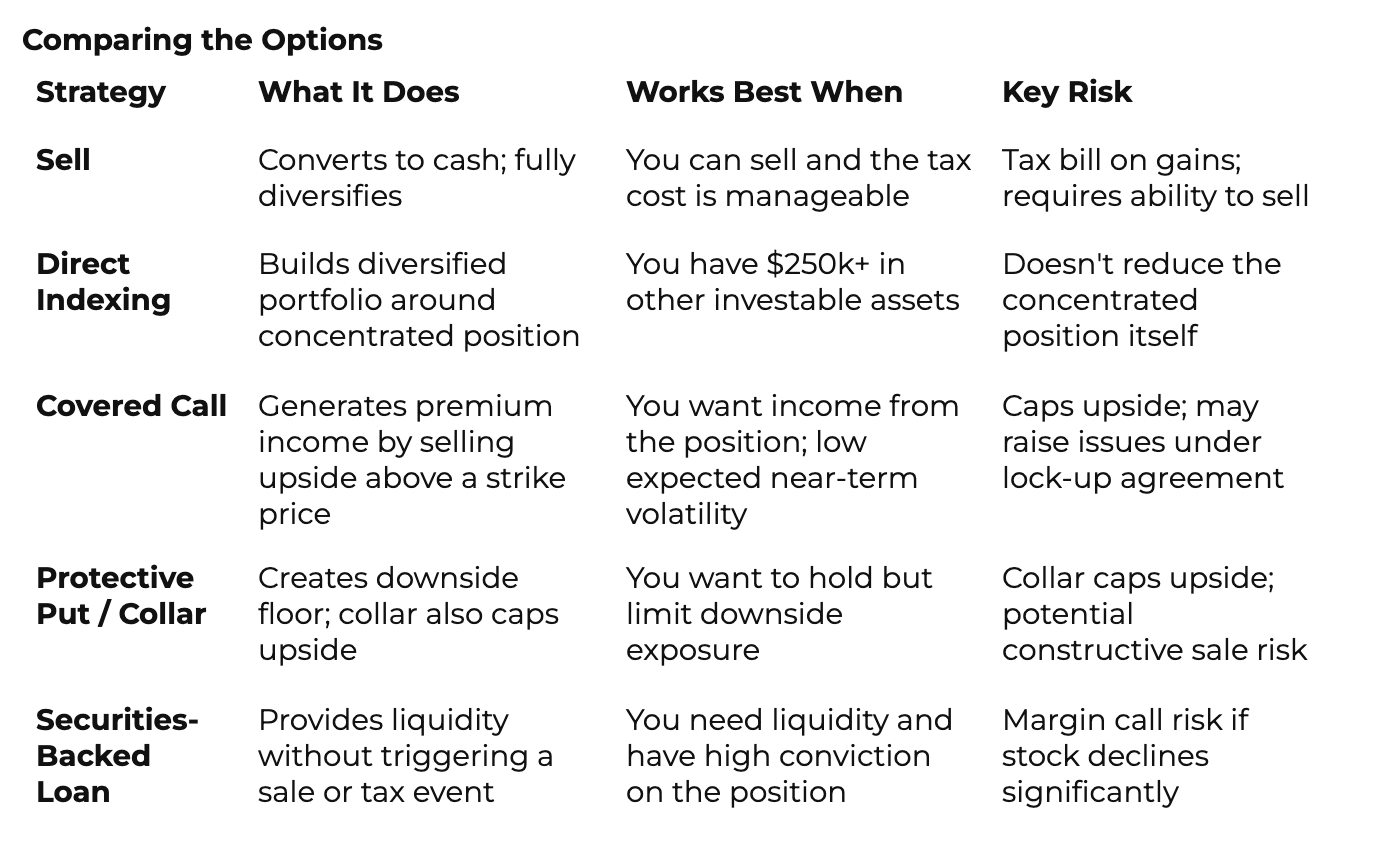

Sell

The most direct answer is still the right one for many situations: sell the shares, pay the taxes, and move the proceeds into a diversified portfolio.

That sounds obvious, but it gets complicated quickly. The tax bill on a large sale can be meaningful, particularly if you've had significant appreciation and your income is already high from salary, bonus, and other vesting. There's also a real psychological piece — selling can feel like abandoning conviction in a company you've given years to. If you're in a lock-up period, selling may not be available to you yet at all.

Those complications are worth taking seriously, though they're often outweighed by a simpler observation: the cost of a tax bill today is almost always less than the risk of watching a concentrated position decline. Selling some is not a failure of conviction, it’s risk management.

Build a Portfolio Around It with Direct Indexing

For people who have meaningful assets outside their company stock, or are willing to sell down a portion of their concentrated stock, direct indexing is a strategy worth understanding.

Instead of selling your concentrated position, you build a separately managed account of individual securities around it. The portfolio is designed to give you broad market exposure while underweighting your concentrated company. Done well, it also lets you harvest tax losses within the portfolio over time, which can be used to offset gains elsewhere in your financial picture.

The result is something more diversified than the concentrated position alone, without requiring you to sell it. This strategy generally requires at least $250,000 to $500,000 in other investable assets to be effective, and it works best the more capital you have to work with. It doesn't reduce the concentration itself, but it meaningfully changes the overall shape of your financial picture.

Beyond Selling: Options Strategies and Lending

For employees who can sell but prefer not to, who are working around a lock-up, or who need liquidity without giving up the position, there are strategies worth knowing beyond an outright sale.

Two things to understand before going through each:

Options on your company's stock require that the stock is publicly traded and that an active options market has formed for it. For new IPOs, options typically become available within a few weeks of listing. If Anthropic or OpenAI hasn't gone public yet, these strategies apply to you in the future, not today.

If you are in a lock-up period: lock-up agreements generally restrict the sale of shares, and whether a specific options strategy constitutes a sale under your particular agreement is a legal question, not a financial one. Before executing any of these strategies, check with your company's legal and compliance team

Covered Calls

A covered call is a strategy where you sell someone else the right to buy your shares at a specified price, called the strike price, by a specified date. In exchange, they pay you a premium upfront.

If the stock stays below the strike price by the expiration date, the option expires without being exercised. You keep the premium and you keep your shares. If the stock rises above the strike price, the buyer exercises their right to purchase your shares at that price. You sell at the agreed price and keep the premium you already collected.

The appeal is income: you generate cash from a position while you continue to hold it, without selling. The cost is a ceiling on your gains. If Anthropic's stock is at $50 and you sell a covered call at a $60 strike, then the stock rises to $100, you sell at $60. You participated in the first $10 of appreciation and gave up the next $40. For a position you hold with high long-term conviction, that trade-off is significant.

Protective Puts and Collars

A protective put is the purchase of the right to sell your shares at a specified price by a specified date. It functions as insurance against a significant decline. If the stock falls below the put strike price, you can sell at the higher, locked-in price. If it doesn't fall, the put expires and you've paid a premium for protection you didn't end up needing.

A collar combines both strategies: you buy a protective put to create a downside floor, and fund it by selling a covered call that creates an upside ceiling. The two premiums roughly offset each other, so the net out-of-pocket cost is small or close to zero. The result is a position with a defined range of outcomes for a specified period.

The reason someone does this: they believe in the position long-term, don't want to sell, and want to limit how much they can lose if things go wrong. A collar is particularly useful when a concentrated position represents a large share of net worth and a sharp decline would meaningfully change your financial situation.

There's an important tax wrinkle here: a collar structured too tightly can be treated by the IRS as a "constructive sale," meaning you could owe tax as if you had sold the position even though you haven't. The rules depend on the exact structure. Get tax and legal guidance before putting a collar on a large, low-basis position.

Securities-Backed Lending

A securities-backed loan, sometimes called a pledged asset line or PAL, lets you borrow against your shares without selling them.

You pledge the shares as collateral, receive cash, keep the shares, and pay interest on the loan. Because a loan is not income, borrowing against your shares doesn't create a tax event. The proceeds can go toward anything: a down payment, other investments, estimated tax payments, liquidity you need now while you hold the position for the long term.

For public shares during a lock-up period, a number of lenders, typically private banks and some brokerage firms, are willing to extend credit, though they generally lend a lower percentage of value against restricted shares than against unrestricted ones. For pre-IPO shares, a smaller number of lenders will extend credit, and the terms tend to be more restrictive and more expensive.

The risk that gets underestimated: if the stock falls significantly, you may receive a margin call, a demand to pay down the loan or post additional collateral. At exactly the moment the position has declined and you feel worst about it, you may need to come up with cash or sell shares at a loss. This is one of the more common ways concentrated positions go wrong for people who thought they had an intelligent hedge in place.

Borrowing against concentrated stock can make sense, but it has to be sized carefully and come with a clear, pre-planned answer to: what do I do if this stock drops 30%? If that answer isn't settled before you execute the loan, the strategy isn't ready.

Why You Need a Plan Built for Your Situation, Not the General Case

None of the strategies above is wrong by default, and none is right by default. The right answer depends on things a general post can't account for: how much of your net worth is in this position, what your full tax picture looks like for the year, whether you have other assets to draw on, what you need the money for, and how you'd actually handle a 40% decline, financially and emotionally.

What we've seen working with clients at companies like Anthropic, SpaceX, and OpenAI is that the decisions made in the first few months after an IPO have an outsized effect on where people end up financially. The strategies themselves aren't the complicated part. The harder part is that those decisions tend to get made under time pressure, with high emotion, and without a clear view of the tax and planning implications. The person who walked in with a framework built months earlier almost always navigates that window better than the person reacting to it in real time.

The goal of a concentrated stock plan isn't to capture every dollar of upside. It's to make sure you don't give back more than you had to: to taxes that weren't modeled, to a margin call that forced a sale at the wrong time, or to a paper gain that eroded while you waited for a better moment that didn't arrive.

If you're holding equity at Anthropic, SpaceX, OpenAI, or another company at an inflection point, we'd be glad to help you think through what a plan built for your situation looks like.

Frequently Asked Questions

Can Anthropic or OpenAI employees sell their shares before the IPO?

In most cases, no. Before a company goes public, shares are generally illiquid. Employees may have the opportunity to sell through company-sponsored tender offers or secondary market transactions, but both are limited in availability and often capped in size. Once a company IPOs, employees typically enter a lock-up period, often six months, during which they still can't sell. Check your grant agreement and any company communications for the specific terms that apply to you.

What happens to my Anthropic or SpaceX stock options during a lock-up period?

A lock-up agreement generally restricts the sale of shares, not the exercise of options. You may be able to exercise vested options during a lock-up period, but you typically can't sell the resulting shares until the lock-up expires. The decision of whether to exercise during a lock-up involves tax planning, cash flow, and risk considerations that are specific to your situation.

Is a covered call or collar allowed during my lock-up period?

It depends on your specific lock-up agreement. Lock-up restrictions vary by company and underwriting agreement, and some structures, particularly collars, can be interpreted as an effective sale under both legal and tax rules. Before using any options strategy during a lock-up, review the terms of your agreement and consult with your company's legal team.

What is a constructive sale, and why does it matter for a collar strategy?

A constructive sale occurs when you enter into an arrangement that eliminates substantially all of the risk of loss and opportunity for gain in a position you still technically hold. The IRS can treat this as a taxable sale even though you haven't sold the shares. Certain collar structures, particularly those where the put and call strikes are too close together, can trigger constructive sale treatment. The rules are detailed, and the tax consequences can be significant.

How much of my net worth should be in one stock?

There's no universal answer, but most financial planners get uncomfortable when a single position exceeds 10% to 20% of net worth, and more so as it climbs beyond that. The right threshold depends on your liquidity, your other assets, your time horizon, and your capacity to absorb a significant loss in that position without it derailing your other financial goals.

Follow our Instagram for personal finance tips and inspiration.

Stephanie Bucko and Cristina Livadary are fee-only financial planners based in Los Angeles, California. Stephanie is the Chief Investment Officer and Cristina is the Chief Executive Officer at Mana Financial Life Design (FLD). Mana FLD provides comprehensive financial planning and investment management services to help clients grow and protect their wealth throughout life’s journey. Mana FLD specializes in advising ambitious professionals who seek financial knowledge and want to implement creative budgeting, savings, proactive planning and powerful investment strategies. As fee-only fiduciaries and independent financial advisors, Stephanie and Cristina never receive commission of any kind. Stephanie and Cristina are legally bound by their certifications to provide unbiased and trustworthy financial advice.