Should You Max Out Your 401(k) or Roth IRA First?

A Mana Guide for High-Earning Tech Professionals and Business Owners

This is one of the most common questions we get at Mana when it comes to retirement contributions. Whether you’re an enterprise account executive trying to figure out what to do with your 401(k) and backdoor Roth, or a business owner staring at the dual contribution limits of a Solo 401(k), the question comes up year after year: where should my next dollar go?

The honest answer—the Mana answer—is that it depends. But “it depends” without a framework isn’t helpful, so we wrote this guide. By the end, you’ll understand the key factors driving this decision, see how it plays out for people like you, and walk away with a clear way to think about the order of operations for your retirement savings.

We’ll walk through the fundamentals, then show you how we think about this with our clients.

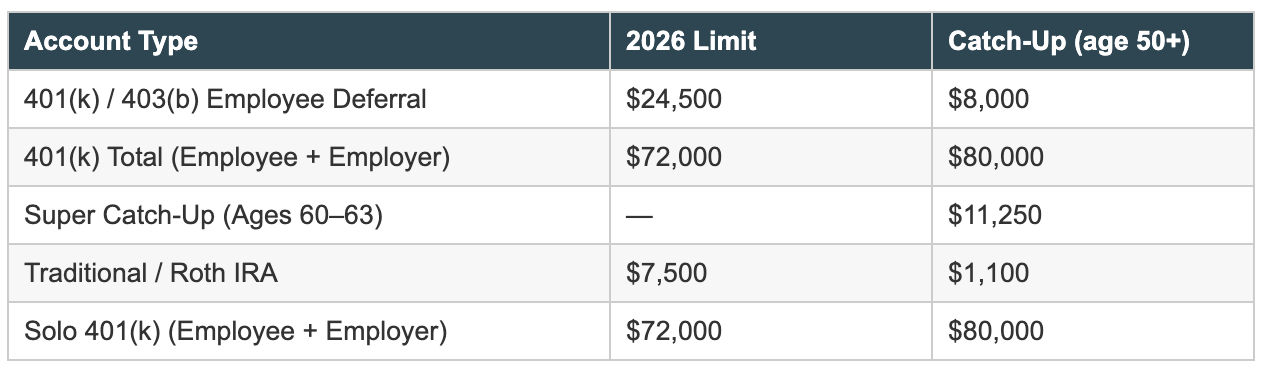

2026 Contribution Limits at a Glance

Before we get into strategy, let’s ground ourselves in what the IRS allows you to contribute this year. These numbers changed for 2026, so even if you’re a seasoned saver, it’s worth a refresh.

A few things worth calling out here. The IRA contribution limit increased to $7,500 for the first time in several years, which is meaningful for backdoor Roth strategies. And if you’re over 50 and earned more than $150,000 in W2 wages last year, your catch-up contributions to a 401(k) must now be made as Roth contributions starting in 2026. This is a SECURE 2.0 change we’ve been preparing our clients for since 2024, and it has real implications for how you structure your contributions. More on this below.

For Solo 401(k) owners, the combined employee-plus-employer limit is $72,000 (before catch-up). That’s a significant amount of tax-advantaged space for business owners who can fund both sides.

The Core Difference: When You Pay Taxes

At the heart of this decision is a single question: do you want to pay taxes now or later?

A traditional (pre-tax) 401(k) contribution reduces your taxable income today. The money grows tax-deferred, and you pay ordinary income tax when you withdraw it in retirement. A Roth IRA contribution (or Roth 401(k) contribution) is made with after-tax dollars—no deduction now—but the money grows tax-free and comes out tax-free in retirement, provided you meet the holding requirements.

The math is deceptively simple on paper: if your tax rate is the same when you contribute and when you withdraw, the outcome is identical. But your tax rate is almost certainly not going to be the same. And that’s where the strategy lives.

Here’s the key nuance that gets overlooked: you contribute at your marginal tax rate (the rate on your last dollar earned), but you withdraw at your effective rate (a blend across all the brackets you fill). For a married couple in retirement whose only taxable income comes from 401(k) distributions, the first ~$30,000 is taxed at 0%, then 10%, then 12%, and so on. That’s a dramatically lower rate than the 32–37% bracket many of our clients are in today.

How Distributions Work in Retirement

Understanding how money comes out is just as important as knowing how it goes in. The distribution rules for 401(k)s and Roth IRAs are fundamentally different, and those differences shape the strategy.

Traditional 401(k) distributions are taxed as ordinary income. Starting at age 73 (thanks to SECURE 2.0), you’re required to take minimum distributions (RMDs) whether you need the money or not. Those RMDs can push you into higher tax brackets, increase the taxable portion of your Social Security benefits, and trigger higher Medicare premiums through IRMAA surcharges.

Roth IRA distributions, by contrast, are tax-free and penalty-free after age 59½, provided the account has been open for at least five years. Crucially, Roth IRAs have no required minimum distributions during the original owner’s lifetime. That means your Roth can continue compounding tax-free for as long as you live—a powerful feature for estate planning and for maintaining tax flexibility in retirement.

Roth 401(k)s are a hybrid. Contributions are after-tax (like a Roth IRA), and qualified withdrawals are tax-free. However, Roth 401(k)s were historically subject to RMDs—though starting in 2024, SECURE 2.0 eliminated that requirement. If you have a Roth 401(k), it now behaves much more like a Roth IRA in retirement.

The retirement planning takeaway: having a mix of pre-tax and Roth assets gives you the ability to manage your taxable income year by year, drawing from the right buckets at the right time. This tax diversification is one of the most powerful levers retirees have, and it’s something we plan for with every Mana client.

What Should Influence Your Decision

There’s no universal answer because the right choice depends on your specific circumstances. Here are the factors we weigh with clients:

Your Current vs. Future Tax Rate

If you’re deep in your peak earning years and expect to be in a lower bracket in retirement, traditional (pre-tax) contributions often win. You’re getting a deduction at 32–37% and will likely withdraw at a blended rate far below that. If you’re earlier in your career or in a transition year—maybe you took a sabbatical, switched jobs, or your income dipped—Roth contributions can be a gift to your future self.

Whether You’re a Super Saver

If you’re saving well north of 20% of your gross income, you may be accumulating so much in tax-deferred accounts that your RMDs will push you into a high bracket in retirement. In that case, leaning more heavily into Roth contributions now—even at a high marginal rate—can be worth it. We see this frequently with dual-income tech couples.

Your Roth 401(k) Option at Work

Many employers now offer a Roth 401(k) alongside the traditional option. If yours does, you can split contributions however you like up to the $24,500 employee limit. This gives you real-time control over your tax diversification without relying solely on backdoor Roth strategies. Keep in mind: employer matching contributions always go into a traditional (pre-tax) bucket, so you’re automatically building some pre-tax balance regardless.

The New Roth Catch-Up Requirement

Starting in 2026, if you’re 50 or older and earned more than $150,000 in W2 wages last year, your catch-up contributions to a 401(k) must be Roth. The law leaves no room for flexibility here. If your plan doesn’t currently offer a Roth option, you won’t be able to make catch-up contributions at all until it does. We flagged this for clients throughout 2025, and if you haven’t confirmed your plan is Roth-ready, now is the time.

State Tax Considerations

If you currently live in a high-tax state like California but plan to retire in a state without income tax, traditional contributions become even more attractive—you’re deducting at your state rate now and withdrawing at 0% state tax later. Conversely, if you’re in a no-tax state now and might move to one with state income tax, Roth contributions lock in that advantage.

How This Plays Out for Mana Clients

Let’s bring this to life with three scenarios we see regularly at Mana.

Scenario 1: The Enterprise Sales Leader

Maya is a 34-year-old enterprise account executive at a major tech company earning $350,000 in total compensation, including RSUs. Her employer offers both a traditional and Roth 401(k) with a 50% match up to 6% of salary.

Maya is solidly in the 32% federal bracket and lives in California. She plans to stay in tech for another 15 to 20 years and expects her income to remain high or continue growing.

Our approach: Maya maxes out her pre-tax 401(k) at $24,500 to capture the deduction at her high marginal rate. Her employer’s plan also allows after-tax contributions beyond the $24,500 employee limit, up to the $72,000 total annual cap. These after-tax dollars can then be converted to Roth inside the plan, a strategy known as the mega backdoor Roth. It’s one of the few ways high earners can get significantly more money into Roth accounts each year, and it’s worth asking your HR or benefits team whether your plan supports it. Maya and her spouse also each contribute $7,500 to Roth IRAs via the backdoor. This gives Maya meaningful tax diversification: the pre-tax 401(k) reduces her tax bill today, while the Roth accounts build a tax-free pool for the future. If she takes a lower-income year down the road (parental leave, a career pivot, early semi-retirement), we’d consider Roth conversions then, when the tax cost is lower.

Scenario 2: The Business Owner with a Solo 401(k)

David is a 45-year-old consultant who runs his own S-corp, earning $250,000 in W-2 wages from the business. He’s building toward a potential business exit in the next five to seven years and wants to maximize his tax-advantaged savings in the meantime. He has a Solo 401(k) and makes both the employee deferral ($24,500) and the employer profit-sharing contribution (25% of wages, up to the $72,000 combined limit).

This is where things get interesting. David’s employee deferral can be either traditional or Roth. His employer contribution is always pre-tax. And because David is over 50 and his W-2 wages exceeded $150,000 in 2025, his catch-up contribution must be Roth in 2026.

Our approach: David contributes $24,500 as his employee deferral on a pre-tax basis, which lowers his current-year taxable income and also has downstream effects on his qualified business income (QBI) deduction. His $8,000 catch-up goes in as Roth, as required by the new rules. His employer profit-sharing contribution of $47,500 goes pre-tax. He and his spouse also fund backdoor Roth IRAs at $7,500 each. This blend gives David substantial pre-tax savings to lower his current bill, while building Roth assets through the mandatory catch-up and backdoor IRAs. In years when business income dips, we might shift more of the $24,500 employee deferral to Roth.

Scenario 3: The Dual-Income Tech Couple with Equity Compensation

Priya and James are both in their early 40s, working in tech sales and product management with a combined income of $600,000, including RSUs and equity compensation. Both have 401(k)s with Roth options, and they’re saving aggressively—north of 25% of gross income.

They’re classic super savers. At their savings rate, their retirement accounts are likely to be substantial by the time they’re in their 60s, which means RMDs could be large enough to keep them in a high bracket even in retirement.

Our approach: We lean a bit more Roth for Priya and James. They each put a portion of their 401(k) deferrals into Roth 401(k), taking advantage of the after-tax “space” inside the retirement account. They both fund backdoor Roth IRAs. The goal here is deliberate tax diversification: enough pre-tax to bring down this year’s bill, but enough Roth to create real flexibility later. We model projected RMDs in their financial plan to calibrate the split annually.

Scenario 4: The Pre-Retiree Planning the Next Chapter

Linda is 58, a VP of sales at a SaaS company earning $400,000. She’s planning to step back from full-time work in the next three to five years. She has $2.4M across traditional 401(k) accounts and a modest Roth IRA balance of $120,000. Her husband recently retired and is drawing a small pension.

Linda’s challenge is that her large traditional balance will generate substantial RMDs starting at age 73, which, combined with Social Security and her husband’s pension, could keep her in a high bracket well into retirement. She also qualifies for the new super catch-up contribution of $11,250 once she turns 60.

Our approach: Linda splits her $24,500 employee deferral between pre-tax and Roth 401(k). She leans heavier Roth than she has in prior years because she wants to build a larger tax-free pool before retirement. She and her husband each fund backdoor Roth IRAs at $8,600 (taking advantage of the 50+ catch-up). We’re also mapping out a Roth conversion strategy for the gap years between when Linda stops working and when Social Security and RMDs kick in. Those lower-income years are a window to convert traditional assets to Roth at a fraction of the tax cost, and that window is where a financial life planner can create the most value.

Mana’s Decision Framework

Rather than a rigid order of operations, we think about this as a decision tree. The right path depends on your situation, but here’s the framework we walk through with every client:

1. Capture any employer match first. This is free money, and it always goes into your pre-tax bucket. There is no scenario where you leave match dollars on the table.

2. Fund your backdoor Roth IRA(s). For most high earners, direct Roth IRA contributions are off-limits due to income phaseouts. The backdoor strategy gets you $7,500 per person ($8,600 if 50+) into a Roth each year. This is relatively small dollars in the context of your total plan, so even if you lean heavily pre-tax elsewhere, these Roth contributions are worth doing.

3. Max out your 401(k) employee contribution. The Roth-vs-traditional split here is where most of the strategy lives. In your peak earning years, pre-tax contributions are usually more valuable. If you’re a super saver, adding some Roth to the mix makes sense. If you have a lower-income year, go heavier Roth.

4. Consider the mega backdoor Roth. If your employer plan allows after-tax contributions with in-plan Roth conversions, this lets you push well beyond the $24,500 employee limit and get more money into Roth. Not every plan offers this, but it’s a powerful tool if yours does.

5. For business owners: fund employer contributions. Solo 401(k) profit-sharing contributions up to 25% of compensation (always pre-tax) can get you to the $72,000 combined limit. This is one of the biggest advantages of being a business owner—the contribution space is enormous.

6. Think beyond retirement accounts. Once retirement accounts are maxed, an HSA (if eligible) and a taxable brokerage account are your next levers. The taxable brokerage offers liquidity and flexibility for early retirement goals or large purchases, and it benefits from long-term capital gains rates.

Importantly, this framework isn’t static. We revisit it annually with clients because life changes—new job, new baby, a business that’s suddenly more profitable, a year where you want to take your foot off the gas. The optimal split shifts with you.

The Bottom Line

You don’t have to choose between a 401(k) and a Roth IRA. They work best together, and the strongest retirement plans use both intentionally. Whether you’re a tech professional navigating equity compensation and RSU planning, a business owner building toward a liquidity event, or a pre-retiree designing the next chapter of your life, the 2026 contribution limits open up real space to build pre-tax and Roth wealth simultaneously. The key is calibrating the mix to your income, your savings rate, your tax situation, and your vision for the future.

This is what financial life planning looks like in practice: designing a structure that gives you choices, so that when you’re ready to step back, slow down, or pivot, your money works exactly the way you need it to. As a fee-only fiduciary financial advisor, Mana helps you build that structure with intention.

If you’d like to explore how this framework applies to your specific situation, we’d love to hear from you.

Follow our Instagram for personal finance tips and inspiration.

Stephanie Bucko and Cristina Livadary are fee-only financial planners based in Los Angeles, California. Stephanie is the Chief Investment Officer and Cristina is the Chief Executive Officer at Mana Financial Life Design (FLD). Mana FLD provides comprehensive financial planning and investment management services to help clients grow and protect their wealth throughout life’s journey. Mana FLD specializes in advising ambitious professionals who seek financial knowledge and want to implement creative budgeting, savings, proactive planning and powerful investment strategies. As fee-only fiduciaries and independent financial advisors, Stephanie and Cristina never receive commission of any kind. Stephanie and Cristina are legally bound by their certifications to provide unbiased and trustworthy financial advice.