Investing For Retirement: Why do it now? How to start? And what if you don’t have a company 401(k) plan?

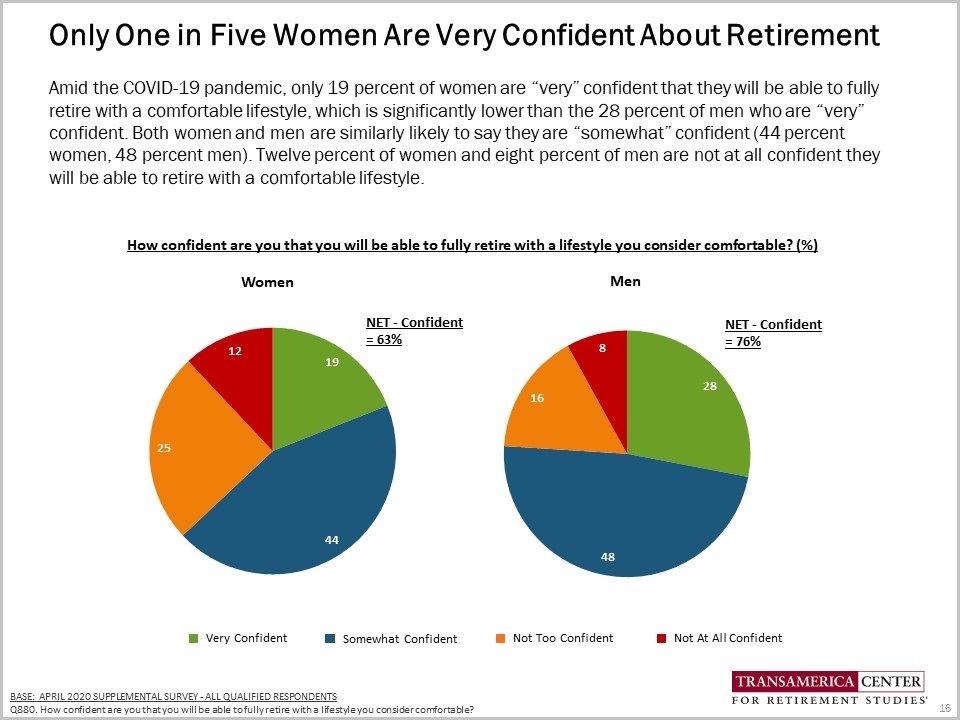

In the future, the idea of ‘retirement’ will likely look very different from the current picture that big financial companies or their advertising agencies paint. Many people realize this, but not everyone feels like they know how to plan for change. According to a recent survey conducted by the TransAmerica Center for Retirement Studies, only one in five women are very confident that they will be able to fully retire with a comfortable lifestyle. The same survey indicated that women are dreaming big, of active retirements, including traveling (67%), spending more time with family and friends (59%), pursuing hobbies (44%), volunteering (28%), and working (26%). Those big dreams require good savings, and good saving starts early.

Much has been written around why it’s so hard for people to save for retirement and we totally get it - if something is 20, 30 or even 40 years away, why start saving for it now?

At Mana, we’re in the business of achieving big dreams for our clients. So, in this post, we wanted to cover a few critical topics to help our readers start thinking about retirement, including 1) why you should start saving, 2) how to do it, and 3) what options you have if your company doesn’t provide a 401k plan.

Why you should start saving now…

Described in its most basic form, retirement is a 30+ year period where you won’t be earning money, but you’ll still want to be living a comfortable life. Our parents and grandparents relied on Social Security as a large portion of their income, but based on the funding projections of Social Security, the likelihood of today’s workforce being able to rely on it is much lower. Last year’s report from Social Security found that benefits would start to exceed the program’s costs in 2020, and the program will deplete its $2.9 trillion reserve fund in 2035. This doesn’t necessarily mean that there will be $0 for you in retirement, but we do think becoming self-reliant is a much safer strategy. Prepare for yourself first, and if you get social security down the road, consider it a bonus!

The points above illustrate the idea that creating a retirement plan is paramount to long-term financial success. The biggest factor in determining how much you need to save for retirement is how much you spend. While your life in retirement might look different than your life today, your current expenditures and lifestyle are a reasonable starting point. In other words, you should assume that your current spending will remain consistent, adjusted for inflation, for the rest of your life.

Here’s an example: if you spend $100k per year today - multiply that over 30 years and you get $3 million before adjusting for inflation. The further away you are from retirement, the more unknowns there are in terms of your future income and expenses, so being directionally correct is a great starting point. Establishing savings of $3 million might sound difficult now, but for those who start saving early and remain consistent in their habits, compound interest works wonders.

Consider these two individuals: Proactive Patty & I’ll Do It Later Larry. Proactive Patty started investing at the age of 30 years old, and she invested $1,625 per month for 15 years until she was 45 years old. She invested in a stock portfolio that returned 7% per year. At the age of 65, she had $2,080,208 in her account. I’ll Do It Later Larry, on the other hand, started investing at age 40 and invested $1,625 per month from age 40 to 65. He invested in the same stock portfolio that returned 7% per year. At the age of 65, Larry had $1,316,367 in his account.

So what happened here? Patty’s total contributions over a 15 year period were $292,500 and Larry’s total contributions over the 25 year period was $487,500. But because Patty invested early and stayed invested, she received the benefit of compound interest. A benefit that earned her over $750k of extra money in retirement than her counterpart who invested $195k more than she did! Compound interest for the win.

How to start saving for retirement…

{kind=link}

Hopefully our examples above have convinced you to start saving for retirement ASAP! Maybe you’re thinking, “okay, sounds great, but how can I do it?”. The next part of this blog post explains how. Here, we’re going to talk through savings strategies for three common scenarios: 1) If you work for a company with a 401k; 2) If you work for a company without a 401k plan; 3) If you work for yourself.

1. Working for a company with a 401k

If you work for a company, the easiest way to get started in saving for retirement is through their 401k plan. A 401k is a tax-advantaged retirement plan that is sponsored by your employer. 401k’s make it easy to save early and often. How a traditional 401k works: you elect a specific dollar amount or percentage of your salary you’d like to save each year, and that amount gets automatically deducted from your paycheck before you pay taxes. For instance, if you’re making $150,000 and contribute 13% (or $19,500) of your pay to your 401k, you’ll be taxed as if you only made $130,500 - lowering your tax liability today.

Note: some companies will have specific restrictions (eg. 3 months from your hire date) on when you can begin participating in the plan, so we recommend checking with HR on the specific details of your plan.

Another useful attribute of company 401k plans is the potential for employer matching. Some companies will match your contributions up to a certain percentage of your salary and/or bonus. Make sure you ask about this with your specific employer. Matching is common; according to SHRM’s 2017 Employee Benefits report, of the 90% of employers who offered a traditional 401(k) plan, 76% provided an employer match. Employer matches mean free money! These matched dollars are money that you don’t have to save in the future. We’ll give an example for someone making $150,000 a year, who is saving $19,500 a year or $1,625 a month (this is the maximum contribution individuals can make in 2020 to their 401k plans). Their employer matches 100% of these contributions, up to 4% of their salary. At the end of the year this person will have saved $25,500 for retirement, with their employer having contributed $6,000 to their 401k! This case enforces the idea that if your employer matches, you should save at least as much as your company matches. At Mana, we prefer all of our clients max out their 401k contributions.

401k contributions are super convenient ways to save, but they might not be enough for people who want to maintain their current expenditures in retirement. Before we move on, a quick note about ROTH 401ks - 7 in 10 companies allow their employees to contribute to their retirement plan with after-tax dollars, but few participants take advantage of this amazing feature. ROTH contributions are made with after-tax dollars, which means that in retirement, you won’t have to pay any taxes when you withdraw from this account. While there are income limits to Roth IRAs (see more about this below) there are no income limits to Roth 401ks. Regardless of your current situation, given the potential for taxes to increase in the future, contributing to a Roth 401k should also be considered as a supplemental retirement savings strategy.

2. What if you work for a company that does not offer a 401k plan?

For this scenario, our first point of advice is: talk to your HR department or leadership about getting a company 401k plan! We’re here as a resource for businesses if you need us.

Nevertheless, here are our two favorite low-cost options for individuals at businesses of all sizes:

Invest in a Traditional IRA

Invest in a Roth IRA

An IRA, or Individual Retirement Account, provides the same tax benefits as a 401k plan. You invest today, and your money grows from now until retirement without any tax implications. In a Traditional IRA, you receive a tax deduction today for the amount you contribute, but when you retire, you will pay taxes on the withdrawals from your account. In a Roth IRA, you receive no tax benefit today for contributing, however in retirement, all of the money and investment growth is yours and tax free. This makes both Traditional and Roth IRAs great options with strong future benefits, but your present day contributions will be limited to a maximum of $6,000 total (in 2020), which means that if you plan to be a $100k/year spender in retirement, investing in an IRA won’t be enough.

If you have the choice, we like the Roth IRA for its flexibility and tax efficiency, but it’s important to know the rules. In order to invest directly in a Roth IRA, you have to make less than $139k per year as a single filer and less than $203k per year as a married filer. Note: just because you make more, doesn’t explicitly prohibit you from taking advantage of the Roth IRA. Find out more in our blog post, You Might Be Rich, But You Can Still Roth.

3. What if you work for yourself?

If you are an employee of a company, or working for yourself, having self-employment income provides several fruitful opportunities for retirement savings. Just as a company can offer a 401k plan, you as a sole proprietor or small business owner can establish your own workplace retirement plan. This includes 401ks, SEP IRAs and SIMPLE IRAs, to name a few. The decision on which plan to select depends on the number of employees you have, the amount of income you earn, and the amount you would like to save on an annual basis. The advantage of each of these plans is that you as a business owner not only receive tax-free growth on your invested assets, but your contributions to the plan also serve as an expense for the business, lowering your business tax bill! There are many paths to optimizing this choice, and we recommend working with a financial planner to determine which one is best for you.

Financial planning is all about trade offs. One of the most important trade offs you can make is to balance your savings for short & mid term goals with that of your retirement. There are a variety of vehicles that can make your retirement assets grow tax-free between now and then. We say, “use them!”. And when possible, max them out. At Mana, we know that it’s not easy to proactively save, but we constantly remind our readers and clients the value of starting early (now!), and being consistent. We recommend that everyone automates their savings, to reduce the cognitive burden of this task. One day retirement will be a short term goal, but planning for it short term won’t work. The reality is that the sooner you start saving, the less you will need to save.

Cristina Livadary is a fee-only financial planner based in Los Angeles, California and is the CEO of Mana Financial Life Design. Mana Financial Life Design provides comprehensive financial planning and investment management services to help clients organize, grow and protect their wealth throughout life’s journey. Mana specializes in advising professionals in the tech industry, as well as women who work in institutional investing, through financial planning and investment management. As a fee-only fiduciary and independent financial advisor, Cristina never receives commission of any kind. She is legally bound by her certification to provide unbiased and trustworthy financial advice.