Retirement's Magic Numbers

You’ve probably been told over and over that retirement contributions are important. But how do you pick the right number? How do you calculate longterm financial benchmarks? And how do you maximize the chance of meeting your retirement needs? In this post, we’ll answer questions about retirement’s “magic numbers” and discuss how to think constructively about your calculations and goal-setting.

A decision you have to make in almost any W2 job is what percent of your paycheck should be allocated to your 401k. For some of you, this decision may also include contributions to two options: a traditional 401k or a Roth 401k. In this blog, we will talk about how to think about your retirement in actual numbers by walking you through an example and then we’ll provide you with details on the types of accounts that exist to enable you to maximize preferential tax treatment.

You might be surprised to find out how much living in retirement could cost. It feels far away, but the reality is that the sooner you start consistently saving, the better. Consistency doesn’t necessarily mean every month; however, it does mean every year as the IRS tax code has been set up for individuals to take advantage of tax breaks on an annual basis.

The first step in figuring out how much you should save for retirement is figuring out how much retirement will cost. How will you know? Spend some time thinking about what you want your life to look like in retirement. At what age does retirement start? What’s a reasonable time frame to expect to live in retirement? While the answer to this question varies from person to person, it might help to have some data to back up your initial planning. The average retirement age in the United States is 61 years old. The average life expectancy in the United States is 79 years; and women have a longer life expectancy of 81 years. If a man and woman are married, the chance that at least one of them will live to any given age increases. There's a 72% chance that one of them will live to age 85 and a 45% chance that one will live to age 90. Armed with these averages, it’s also important to consider how long your parents and other close relatives lived. If one of your parents lived beyond 90, it’s a good idea to plan to have your retirement assets last at least that long. As financial planners, we find it important to project out a retirement of at least 30 years to mitigate longevity risk. Longevity risk, or the risk that you outlive your savings, is one of the key factors to control for when constructing your retirement plan.

In our example, we are assuming a couple is planning for an ‘average’ retirement age from age 60 to 90. Knowing they have 30 years in retirement, we must plan to have sufficient income for this time period. Understanding sufficient income means understanding costs. We examined their last 3 months of expenses to find that they spent $30k over the past three months. That would mean an annual living expense of $120k, or $10,000 per month. This monthly spending average is really important - we’ll tell you why in a second. So now let’s project!

In order to enable you to be able to replicate this exercise, we used a free online calculator by Nerd Wallet to come up with projections using the example of $10,000 monthly spending, retiring at age 60 and living to 90. If you’re following along, you can enter your own data on the site:

Enter your age.

Enter your pre-tax income (your salary).

Enter your savings: this should include your 401ks, IRAs and other savings that you want to earmark towards retirement. If a large portion of your net worth is in stock compensation, we recommend earmarking 50% of your company stock to retirement as a starting point.

Enter what you are currently saving.

And then click Optional. Instead of subscribing to the “rule of thumb” of 70% of your pre-retirement income as your “Monthly Retirement Spending”, we recommend you enter 100% of your current monthly average spending (the number you just calculated). While you may have paid off your mortgage, health care costs and travel expenses oftentimes replace this monthly amount.

Depending on how old you are, how much you will need to retire will change. We have mapped out the cost of retirement given our example:

Why does someone who’s 30 need to save $3 million more than someone who is 60? As we move up in age, the cost of retirement decreases (but of course, the time to retirement decreases!). This is because of inflation. Inflation is an economic concept that captures increases in our cost of living. For example, a loaf of bread today costs $5, but in 30 years it might cost $10. Over history, good and services have gotten more expensive. So, for two people with equal living expenses in today’s dollars, a longer time between today and retirement means that your retirement costs will be more expensive. The existence of inflation makes the argument for investing your retirement ever so important. If you kept your retirement in cash, it would actually lose value. You would see the same dollar amount, but in 30 years’ time, those dollars would have less purchasing power.

As an older person, you need to save less OVERALL for retirement, but if you have not started saving, your annual savings will be higher than someone younger.

Using a calculator like this will help you figure out how much is necessary to save for retirement. The next step is to make sure you are maximizing your retirement vehicles. 401ks, IRAs and HSAs are types of accounts that offer preferential tax treatment. By minimizing your taxes, you can maximize your savings for retirement.

Retirement plans and how much you can contribute

Most employers will offer 401k plans. The maximum you can contribute to your 401ks this year is $18,000. For individuals over 55, you are able to contribute an additional $6,000. This number typically increases every year - allowing individuals to save a little more with beneficial tax treatment as the cost of living increases. Maximizing the amount you contribute to your 401k is often the best way to save for retirement. If your employer matches your contributions, you should at a minimum invest into your 401k up to this matching amount.

You may be offered to invest in a Traditional 401k or a Roth 401k. The primary difference between these two are how taxes are treated. When you contribute to a 401k, you lower your taxable income. For example, if you made $100,000 per year and you contributed $10,000 to your Traditional 401k, you would be taxed as though you only made $90,000, because your $10,000 contribution is a pre-tax deduction. If your effective tax rate was 20%, you would be able to save $2,000 (or $10,000 x 20%) on taxes this year. When you eventually withdraw money from your Traditional 401k in retirement, you will be taxed on it as ordinary income. The benefit is that you lower your taxes today and your investments grow tax free. The downside is that you will pay taxes on the distributions in retirement. In a Roth 401k, you are contributing after tax. The benefit for Roth 401ks is that you pay the tax now and then when you withdraw in your retirement in the future, your withdrawals are tax free.

There are multiple schools of thought in terms of choosing a Traditional vs. Roth 401k, but really there are two main variables that drive these decisions: 1) your current tax rate vs. your future tax rate, and 2) the US tax rates now vs. the future. Diversifying your risk to these two factors by contributing to both types of accounts is one way to not have to worry about the details. The main point - invest as much as you can into these retirement accounts! Saving earlier for retirement means that you have to save less money each month and will provide you with way more flexibility and freedom down the line.

Beyond the 401k plan, all individuals are able to contribute to Individual Retirement Accounts, or IRAs, but should be careful to monitor the tax rules on these accounts. Similar to the 401k structure, IRAs offer preferential tax treatment to help individuals save for retirement. The maximum contribution to Traditional and Roth IRAs in 2019 is $6,000. Traditional and Roth IRAs work similarly to their 401k counterparts in terms of taxation, however, if you are an are an active participant in a company 401k, your contributions may not actually be tax deductible. In order to contribute to a Roth IRA, you have to make less than $135k as a single person or $199k as a married couple filing jointly.

Just because there are restrictions on tax deductibility doesn’t mean IRAs should be ignored for W2 employees. There are strategies that can be deployed to help individuals minimize their taxes and maximize their contributions to these accounts, such as a backdoor Roth contribution or a mega backdoor Roth contribution. Recent changes in the Tax Cuts and Jobs Act have mitigated some of the concerns around using these strategies, but it is important to understand the regulations and tax code as you navigate. We recommend working with an advisor or CPA / tax consultant to help you strategize on these accounts.

If you’ve maxed out retirement accounts, are you done saving for retirement?

The short answer is, probably not.

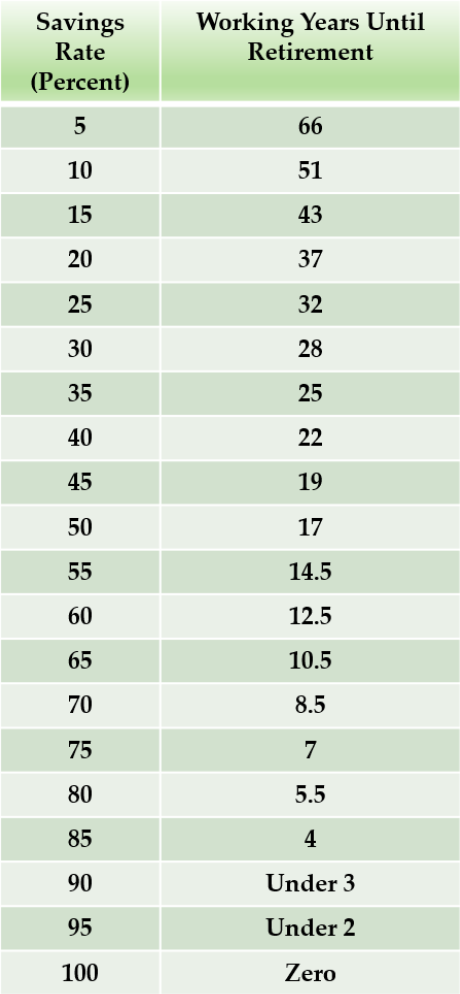

Mr. Money Moustache has put together a simple way to think about the percent you should be saving based on your current income, shown in the table. Let’s assume you are 30 years old and have 30 years left until your 60th birthday when you plan to retire. Your savings rate should be 28%.

If you are currently making $150,000, this would be an annual savings of $42,000. Since the maximum contribution to your 401k plan is $18,000, there is an additional $24,000 of savings to be allocated.

Some other options?

Health Savings Accounts. Health Savings Accounts are actually considered the most tax efficient account - oftentimes referred to as ‘triple tax free’.

Your contributions are tax deductible.

Your investments grow tax free.

Your withdrawals are tax free, assuming you use them for qualified medical expenses.

With these great benefits, contributing to a Health Savings Account is a way to save for your retirement, specifically to fund your health needs in retirement. Qualified medical expenses include things like going to the doctor, prescription drugs, or other out of pocket medical expenses, but can also be used to cover long-term care insurance, health care continuation coverage (such as coverage under COBRA), health care coverage while receiving unemployment, or medicare and other health care covered if you are 65 or older. Contributions to an HSA are limited to $3,500 for a single person and $7,000 for a family in 2019. If you are over 55 anytime in 2019, you can contribute an additional $1,000.

But we still have to save more. Now what?

Tax advantaged vehicles an excellent way to start, but this doesn’t mean that you are limited to saving that way. When savings rates required exceed what is allowed in these accounts, creating a brokerage account with a portion dedicated to your retirement enables you to save without limitations. While the account itself doesn’t receive the same tax benefits, there are investment strategies that can be implemented to help mitigate the taxes you pay along the way. For example, there are tax efficient investments that can be used in a taxable portfolio, while your retirement accounts hold less tax efficient investments. Tax loss harvesting and rebalancing are other ways to help mitigate your overall investment tax exposure.

The main point: there are no magic numbers or uniform guides.

Everyone’s work experience, stage of life, and long-term goals are different; so everyone’s retirement plan should be unique.

However, there are some good heuristics/planning steps to follow:

Start by figuring out how much you should save, and then make that goal a priority.

1) Take inventory of your current investments and determine what should be earmarked for retirement. Don’t forget those old 401ks, a portion of your stock compensation, and any rental real estate property.

2) Maximize your investments in tax advantaged vehicles first, including 401ks, IRAs and HSA! Consult a financial advisor or CPA to determine how to utilize strategies outside of normal contributions.

3) If you have maxed out your retirement accounts, it doesn’t mean you shouldn’t be saving. Save and earmark a portion of your taxable investments to retirement.

It may be 10, 20 or even 30 years away, but proactively planning (in the right accounts), saving (an appropriate amount) and investing (in a diversified portfolio) is important no matter what stage of life you are in.