Bonds and Banking: A worthwhile lesson on financial awareness!

Recently, I found myself in a position of banking naivety. After more than a decade of work in finance, this was a surprising experience - but also a great chance to learn and share some important information with our Mana FLD blog readers. The topic: savings bonds! While I have a great grasp of the risk vs. reward of buying Treasury Bonds in today’s market, my last visit to the bank showed me how much more I needed to know about their counterpart: Savings Bonds (bonds that we most likely received from our parents and grandparents in our younger years and, if you’re like me, haven’t thought much about).

While I may have been naive, I am the kind of person that loves to ask questions until I understand a given domain or scenario. I actually have lots of practice developing this skill, because a critical part of my early career was asking the right kinds of questions. My first job was auditing hedge funds, which meant that I had to become an expert in each hedge fund domain, in order to provide investors with assurance that the work they did and the numbers they reported were legitimate. My next job was performing operational due diligence on hedge funds (approximately 500 funds in over a three year career), and writing 40-60 page ‘book’ reports, explaining my findings and opinions, on the funds that made it through our process. I still hold this inquisitive spirit, so I was excited to learn how to deposit Savings Bonds and to be able to share it with our clients. Don’t worry - this won’t be a 40-60 page report - I’ve synthesized the key points below.

Some useful lingo and definitions for this blog post:

Bond - It’s a promise to repay in the future, plus interest.

Maturity - It’s the time when interest stops being paid on the borrowed money.

Some recommendations on how to read this piece:

Find your Savings Bonds and lay them out on your desk.

Read along and match the dates to what we describe below.

Use the calculator to see what you’ve got.

Take action and deposit those matured bonds!

What is a Savings Bond?

It is a financial instrument that is offered by the United States government and is backed by the full faith of the US government. Savings Bonds (along with other bonds like Treasury Bonds that are offered by the US Government) are considered to be one of, if not, the safest financial instrument in the world.

Today, you can only buy treasury bonds electronically (a change that was made in 2012), but in this post I’m going to focus on the paper version because that’s usually what’s sitting in some dusty folder in your file cabinet. The one exception is if you have a tax refund, you can request to receive it in paper Series I Bonds. (Isn’t there just always an exception!?)

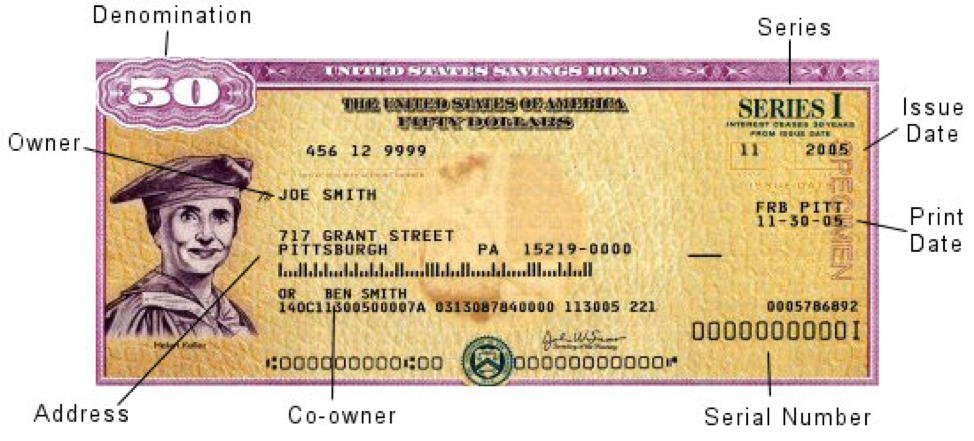

Here’s an example of a Savings Bond:

Let’s walk through the most important things you see on the face:

Owner - that’s you! The social security number written above should also be you, but I’ve seen some older bonds that have the gifter’s social security number on them.

Series - this one is super important! The Series dictates the face value or denomination of the bond. I’ll talk about this more below.

Issue Date - this one is also super important! The Issue Date dictates the calculation used to calculate the interest rate, when interest is paid, and the timing of maturity.

Serial Number - like with any form of identification, this is the ID number of your specific security.

My understanding of Savings Bonds was that they mature over 30 years, pay interest rates that depend on current market interest rates, and are guaranteed to double over that time frame even if the interest didn’t keep up. What I realized is that this is only true for some of the bonds.

So, let’s break it down:

Generally speaking, these bonds will pay you interest (not in cash, but by adding to the cash redemption value of the bond) over a 30 year period. Because of their long term time frame, your intended goal should be to hold these for the long term. You are able to cash them out after 12 months with a penalty or after 5 years without penalty; but, when you cash them out, you forego any future interest.

They earn interest on a monthly basis, but it is compounded (or added to the value of your Savings Bond) twice per year. You can find out when your bond compounds interest using the calculator I’ll talk about - but for the sake of an example, let’s say if you bought a bond in January, it would pay interest in July and again in January. If you cash out this bond in June, you will forego the 6 months of interest paid in July.

Any interest you earn is taxable at the Federal level, but not at State or Local level. You can elect to pay tax on an annual basis OR upon the earlier of cashing out the bond or the bond’s maturity.

Those are the basics, but with those alone, your deposit at the bank might get messed up (like mine almost did). Let’s jump into the two things you need to know as to not get bamboozled by the bank: the Series and the Issue Date.

The series of the bond is a great place to start. Since 1935, the US Government has issued tons of different series of bonds. You would hate me if I dug into all of them, so I’m going to focus on the two most prevalent in more recent history: Series I and Series EE.

The most pronounced difference between these two bonds is their starting point - or the comparison between what you paid for them and the face value (or Denomination as per our picture above).

Series I - You bought at 100% of their face value. If the bond says ‘$50’ on the front of it, you paid $50 for the bond.

Series EE (Pre-2011) - You bought at 50% of their face value. If it says ‘$50’ on the front of it, you paid $25 for the bond.

Series EE (2012 and beyond) - You bought at 100% of their face value. If it says ‘$50’ on the front of it, you paid $50 for the bond. (They really should have named this Series something else!)

It’s no wonder that Series I is the most recent version of these bonds, because it’s definitely the more straightforward. Series I bonds pay a fixed rate of interest that you know when you buy the bond, plus an inflation rate that is calculated twice per year. Every 6 months, you can find your interest rate on Treasury Direct.

Series EE on the other hand is highly dependent on the month and year that it was issued, so now let’s talk about the Issue Date. We’re going to throw a bunch of numbers at you for education purposes, but don’t worry - there is an online calculator for this - and we’ll explain how to use it soon!

Series EE Bonds Issued Before May 1995

You paid $25 for a $50 bond. It had a guaranteed rate of return for a specific maturity period, as identified in the table below. The interest rate was dependent upon prevailing market interest rates at that time (yes - we had super high rates in the 80s!) and the maturity date was dependent on how long it would take the bond to double. There’s a financial trick called “The Rule of 72”, which helps you calculate what percentage return you need in order to double your money over a specific period of time. For example, if you earned 9% per year, it would take you 8 years (or 72 divided by 9) to double your money.

After these bonds reach their original maturity (the column on the right), their rate of interest can take one of two forms: 1) a guaranteed rate of interest for extended maturity; or 2) at a market-based rate (85% of 6-month averages of 5-year Treasury securities yields).

Series EE Bonds Issued Between May 1995 and April 1997

You paid $25 for a $50 bond. The interest paid on these bonds depends on how many years you have held them and the prevailing market rates of interest. Years 1-5 of holding the bond, you’re paid the prevailing short-term interest rate. Years 6-17 of holding the bond, you’re paid the prevailing long-term interest rate. Years 18-30, you fall into the extended maturity period. You should be paid the prevailing long-term interest rate, but this is subject to change.

Series EE Bonds Issued Between May 1997 and April 2005

You paid $25 for a $50 bond. The rate of interest is variable based on prevailing market interest rates, but the Treasury guarantees that your bond will double in value over the original maturity period. For bonds with issue dates from May 1, 1997 through May 1, 2003, the original maturity is 17 years after the issue date. For issue dates from June 1, 2003 through April 1, 2005, the original maturity is 20 years after the issue date. If the rate of interest didn’t keep up with doubling your money, the Treasury will do a one-time adjustment to make up the difference.

Series EE Bonds Issued Between May 2005 and December 2011

You paid $25 for a $50 bond. The rate of interest is variable based on prevailing market interest rates, but the Treasury guarantees that your bond will double in value over the original maturity period, which is 20 years. If the rate of interest didn’t keep up with doubling your money, the Treasury will do a one-time adjustment to make up the difference.

And that was the last of paper Series EE Savings Bonds!

So what’s next? How do you take action?

First, like anything with financial planning, it’s great to take inventory.

Go to Treasury Direct to calculate the value of your bonds. You are able to enter the Serial Number, but you don’t actually have to in order to find the value of the bond. You will just need to know two key pieces of information: Series & Issue Date.

I am going to show a few examples based on the time frames we talked about above:

Once you have your list of inventory, fill out the backs of each of your Savings Bonds that you would like to deposit into the bank. Any bonds that are already matured are worth depositing, as they are not generating any additional interest. For bonds that have not yet matured, I suggest speaking with a financial advisor to determine what the best course of action is for your financial situation.

The information you need to include is a) your address and b) your social security number. You will need to sign the back as well, but we recommend doing this at the bank, as the person at the bank will need to verify your signature. They will most likely ask for your ID and then they will fill out the back and sign to confirm they have verified your identity and run the bond through the system.

The bank is able to process up to 10 treasury bonds at once for direct deposit, which would hit your bank account similar to any kind of check, in about 1-2 days. If you have more than 10 treasury bonds, the bank is able to deposit them, but your entire deposit will be sent to your account by mail after being processed by the treasury (a process estimated to take 3-4 weeks), so you are likely better off making multiple trips to the bank.

Ask the bank teller to provide you with the receipt detail that includes a list of each of the bonds deposited. This receipt should include the following details:

Series

Serial Number

Issue Date

Denomination

Interest

Current Value

Confirm that these details are correct against your inventory. When I went to deposit, the bank teller indicated that my $11,500 of Savings Bonds was worth $9,500. However, she had mislabelled two of the checks as “Series EE” versus “Series I”.

When she made the correction, the deposit amount was over $17,000! I fear to know how many individuals have experienced something similar...

The last step is to make sure you’ve paid tax on these Savings Bonds. On the positive, there are no State or Local Taxes associated with interest on Savings Bonds, but for Federal - taxes are due either when the bond matures or when you cash it out.

A gift worth understanding.

Savings Bonds are a great way to save in a low risk investment that will grow gradually over time. It has the attribute that works well in terms of behavioral finance - “out of sight, out of mind” - so probably not spending it! But if you got these from your grandma or grandpa over 30 years ago, these bonds have matured and are no longer growing. At Mana FLD, we’d encourage you to reinvest into something new.

I hope you learned some of the facets of how these work, but most importantly to check the work of your bank teller - because mistakes can happen!

Stephanie Bucko is a fee-only financial planner based in Los Angeles, California and is the Chief Investment Officer of Mana Financial Life Design. Mana Financial Life Design provides comprehensive financial planning and investment management services to help clients organize, grow and protect their wealth throughout life’s journey. Mana specializes in advising professionals in the tech industry, as well as women who work in institutional investing, through financial planning and investment management. As a fee-only fiduciary and independent financial advisor, Stephanie never receives commission of any kind. She is legally bound by her certification to provide unbiased and trustworthy financial advice.